DWF Ventures: 31 billion United States dollars (US$) RWA, who captures tokenization value

Author

Original link:

https://x.com/DWFVentures/status/206940512319873739?s=20

Summary of highlights:

*Over $31 billion of monetized assets have been deployed in the chain, but only about 10 per cent of them enter DeFi as active TVL. Most assets remain in their wallets for extended periods of time after their monetization, with little further flow to downstream agreements and generating additional value。

*The growth of monetized assets comes from both new inflows of funds and the transfer of encrypted primary capital to the configuration of more robust returns. The bottom reserves of large stabilizers have created significant exposures to United States Treasury bonds, and the new wallet data also show that monetization continues to attract net new users to markets。

*There is still significant room for value release for encrypted infrastructure projects that can address critical issues such as risk management, pricing mechanisms or settlement efficiency, or complete vertical integration systems from the bottom。

*CURRENTLY, 94 PER CENT OF THE MONETIZED ASSETS ARE STILL DENOMINATED IN UNITED STATES DOLLARS. EMERGING MARKET SOVEREIGN BONDS AND REGIONAL PRIVATE CREDIT MARKETS IN THE MIDDLE EAST AND THE ASIA-PACIFIC REGION (MENA/APAC) STILL HAVE SIGNIFICANT GROWTH POTENTIAL。

The wave of monetization has accumulated over the past few years and has accelerated further in the near future with the massive upswing of institutional funds. The core value of adopting a chain infrastructure can be found in many ways, including faster settlement efficiency, greater liquidity, round-the-clock cross-border market access, portfolioability, wider participation opportunities and greater transparency. As funds continue to flow, a key question emerges: who is capturing the value created by monetization

To date, the main beneficiaries of the monetization wave still appear to be traditional financial institutions, rather than encrypted start-ups that have long built the base infrastructure. The report will explore the flow of value in the context of the monetization industry chain, the critical gaps in the current market and how encryption infrastructure can be retained and added value by filling those gaps。

Current status of monetized assets

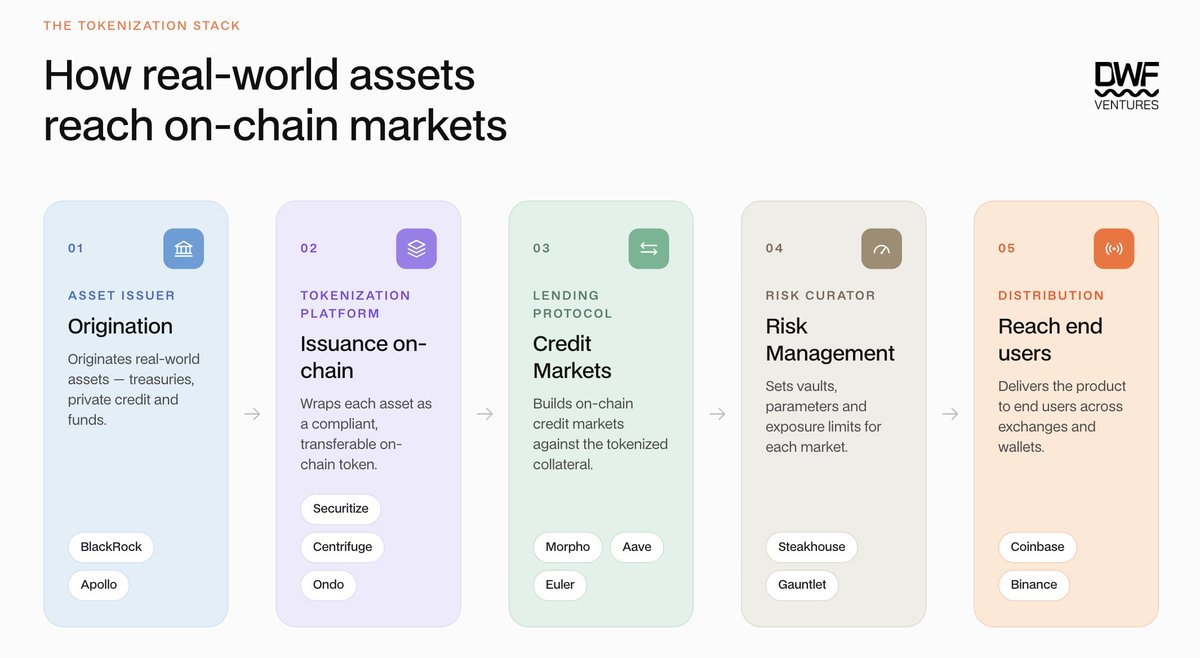

The complete chain-based monetization ecology consists of multiple participants with different functions. While traditional financial institutions mainly cover the chain of asset issuance and monetization platforms, lending agreements, risk management platforms and exchanges constitute an encrypted primary infrastructure layer that provides wider distribution channels and applications for monetized assets。

In practice, however, much of the value remains at the level of a monetization platform, which is not yet fully moving downstream to encrypted ecology. Some monetized assets are subject to issuance or transfer restrictions, foreclosure cycle delays, and KYC requirements, which are fundamentally compatible with the unlicensed DeFi system, thus limiting its further circulation and application throughout the value chain。

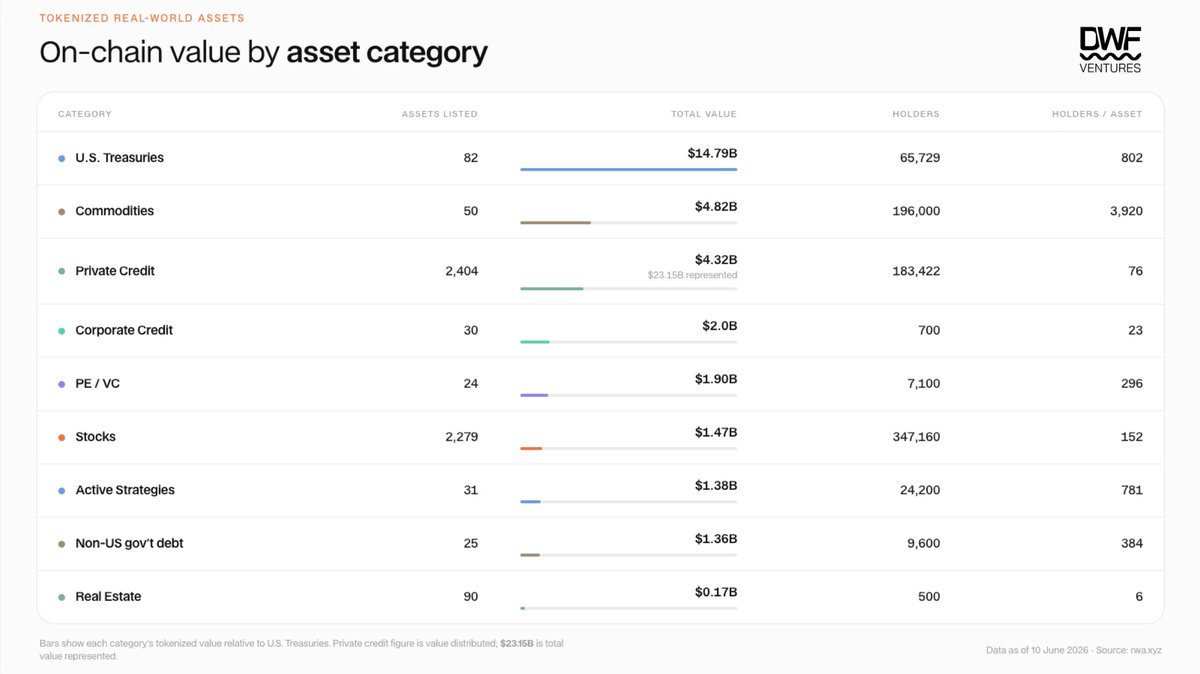

The total size of monetized assets (excluding stable currency) in the chain has exceeded $31 billion, increasing by about 50 per cent since the beginning of the year. This increase is largely driven by the continued inflow of institutional funds, which are accelerating the monetization of assets such as United States Treasury bonds and private loans。

Despite significant increases in the total size of assets, there are significant differences in the distribution and circulation of holders between asset classes. United States Treasury bonds and bulk commodities are in the lead in the number of holders, while the introduction of private loans and real estate remains relatively slow. In terms of circulation, the chain activities of most assets are equally limited. It is estimated that less than 30 transfers per month have been made to United States Treasury products, such as BuIDL, WTGXX and Benji. This is mainly related to regulated access mechanisms and the availability of secondary liquidity, which affect the portfolio and usefulness of assets in DeFi and are directly related to the number of holders. It is estimated that only about $3 billion of monetized assets (about 10 per cent of the total value) are currently present in DeFi, in the form of active TVL, and are concentrated mainly in United States Treasury bonds and bulk commodity assets. Nevertheless, it has created significant value for RWA-related agreements (in addition to asset initiation and distribution platforms), including Sky, Morpho, Aave, Maple and Pendle, which are generating significant trade and revenue from these monetized assets。

However, how many of these inflows came from net additional capital? A significant part of the growth in the United States dollar-denominated market stems from the diversification of reserve asset and fund allocation strategies following the decline in DeFi returns by major agreements and DAO. Sky (former MakerDAO) was one of the first drivers of this application, and there are still over $1.5 billion in monetization funds, such as the BuIDL, deployed in BlackRock. Ethena will also soon be allocated more than $250 million to the AAA CLO fund in Securitize as one of the bottom-up USDe support assets. The growth of such assets can be seen as a “scrambling” of encrypted capital to secure assets, but further analysis will provide a more complete picture。

Chainalysis ' in-depth analysis of wallet activity shows that over 400,000 wallet addresses holding RWA assets received their first RWA token within a week of being created. The wallets had previously had no record of the activity of encrypted assets, indicating that additional capital was entering the market. At the same time, older wallets with a record of past-chain activity are more involved in monetized assets such as bulk commodities and stocks。

Infrastructure gaps in the market

The core value propositions for placing assets in chains have been clear: programmable settlements, portfolio mortgages and a running secondary market. The asset classes that benefit most are often areas where mobility is poor, such as private loans and real estate. However, liquidity tends to be inversely related to potential benefits — assets most in need of chain liquidity, which is precisely the least liquidity available。

The problem of secondary liquidity is intrinsically characterized by several structural obstacles: lack of a well-developed pricing infrastructure, slow settlement of bottom assets and regulatory requirements such as KYC/qualified investor certification. These factors together contribute to the low attractiveness and viability of monetized assets in DeFi. As a result, a variety of solutions to liquidity problems have emerged in markets:

• Sttablecoins as a collateral layer: incorporating tokenized assets into the collateral system allows users to gain gains while increasing their chain mobility. In essence, it is a wrapper mechanism. According to the Pantera State of Tokenization report, it is this mechanism that has resulted in the utilization of 64.3 per cent of less liquid assets such as private loans in DeFi. Maple Finance is particularly prominent in this field, with its syrupUSDC and syrupUSDT TVL already exceeding $3.6 billion。

however, this model has a higher risk exposure, as users have no control over the bottom asset allocation and transparency and the certification of reserves are dependent on platform disclosures. the default event is not non-existent and the user will bear the main risk of first-level loss。

• Refinement of the pricing/pregnancy infrastructure (Improving infrastructure/oracle infrastructure): Private lending and real estate assets rely on regularly updated NAV data, which usually can be updated only once a day at most. This has made it difficult for marketers to effectively hedge risks and thus to provide a narrower price difference in markets with real liquidity. The problem also affects the LTV level of assets and significantly erodes the rate of return when adopting strategies such as recycling leverage. Third-party management agencies with asset allocation and risk management capabilities are often involved in lending platforms such as Morpho and Euler, thus helping to reduce price differentials。

Prophecies such as Pyth Network and RedStone are trying to fill this gap by supporting the pricing of monetized assets by serving round-the-clock monetized stock and bulk commodity markets and providing verifiable real-time price signals. A combination of asset risk rating systems provided by third-party agencies, such as Credora, would significantly enhance market confidence and portfolioability. At the same time, it has helped marketers to complete asset pricing more effectively and to improve the trade differentials for lower-level assets。

• Introduction of a new foreclosure mechanism: prompt settlement was one of the key advantages of the chain. The reality, however, is that chain liquidity is still insufficient to support large-scale transactions, while the off-site market (OTC) is highly fragmented and open mainly to institutional investors. In the case of the United States Treasury debt product Ondo Finance USDY, which provides secondary market transactions, the average slide point reached about 0.2-0.3 per cent, even with a conversion of only $1,000. This means that users still have to rely on T+1 or T+2 settlement mode when they actually exit。

Symbiotic is solving this problem by constructing Liquid Lane. The programme uses a shared treasury infrastructure and, through the RFQ mechanism, buys off competitive offers from market vendors, thereby achieving faster implementation and reducing asset spreads. At the same time, the treasury infrastructure allows funds to be deployed to the lending pool market, bringing additional revenue sources to the LP。

• Vertical integration within a single platform: most issuers of monetized assets continue to rely on external NAV regulators, third-party prognostics and stand-alone trading platforms to complete asset pricing and flow. Figure, on the other hand, has adopted a completely different model at three key stages of the entire chain of internal control: asset initiation (by Provence Blockchain, more than $21 billion has been issued in HELOC), secondary market price discovery (Democratized Prime Dutch auction market) and primary settlement currency (YLDS, the first interest-bearing stable currency registered with SEC). With first-hand data on borrowers ' credit position, LTV ratios and default rates, Figure has a clear advantage in asset pricing。

At present, Figure is expanding this model further through Forge, opening full chains from asset initiation to settlement to underserved asset classes such as real estate equity, automobile loans and trade finance, which may drive rapid growth in new markets。

An important opportunity for the next phase

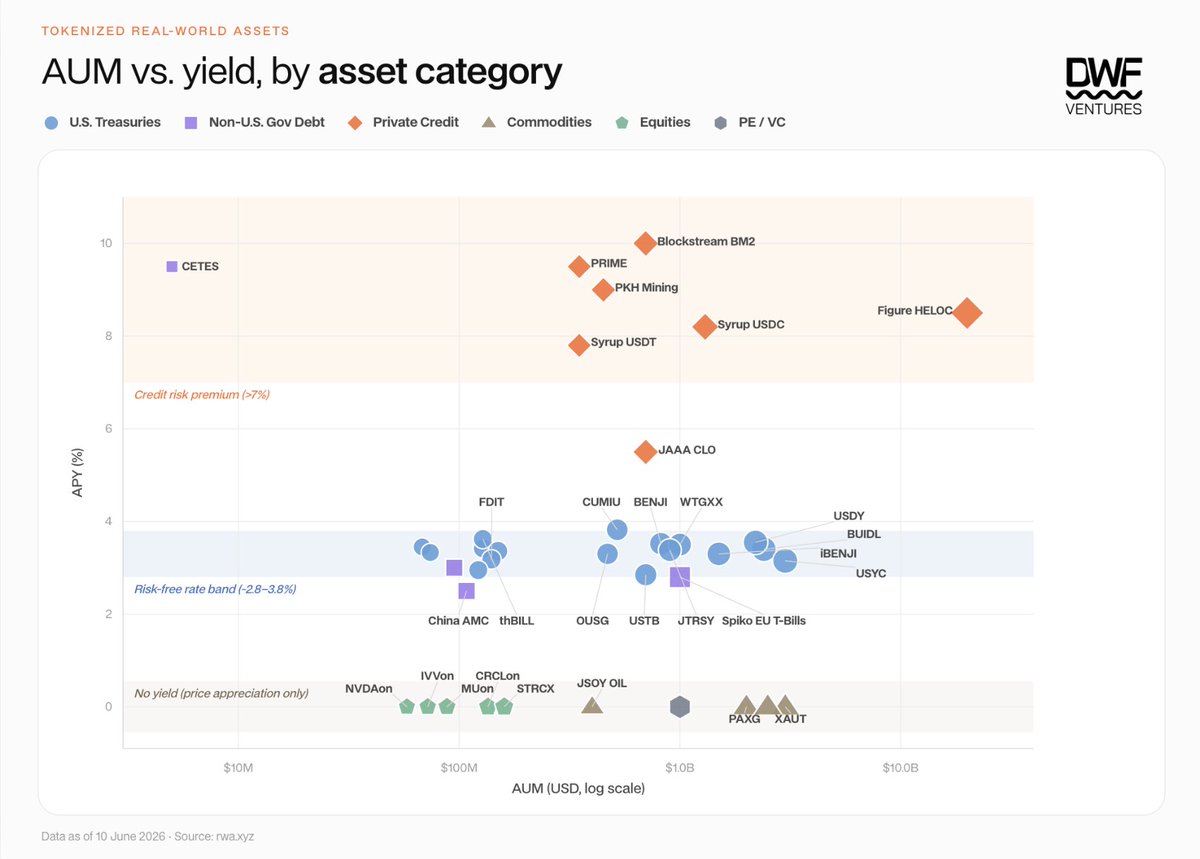

AN ANALYSIS OF THE CURRENT AUM, WHICH MONETIZES ASSETS ALONG THE CHAIN, AGAINST THE RATE OF RETURN BY ASSET CLASS REVEALS THAT SIGNIFICANT DEVELOPMENT OPPORTUNITIES REMAIN IN SOME AREAS. THE FIGURE BELOW SHOWS MARKET DEMAND UNDER THREE DIFFERENT INCOME CHARACTERIZATIONS:

• Credit risk premium (> 7 per cent): Private lending dominates, with returns maintained as AUM grows, relying mainly on vertical integration models (e.g. Figure's HELOC business) or deleveraging through DeFi (e.g. syrupUSDC/syrupUSDT)。

• Risk-free interest rates (3-4 per cent): The sources of income are highly homogenous and competition is concentrated on distribution capacity and portfolio。

• No gain (0 per cent): Assets themselves have strong demand, and chainization mainly provides investors with open access to prices。

In our view, the next important opportunity is concentrated in two main areas: private loans/bonds denominated in non-United States dollars, and the provision of chain earning capacity for bulk commodities and equities。

More than 94 per cent of the monetized assets are denominated in United States dollars, while more than three quarters of the remaining 6 per cent are concentrated in Spiko ' s Euro Treasury Bill Fund. This contrasts sharply with traditional fixed-income markets, which account for more than 45 per cent of the global market size of non-dollar sovereign bonds. Emerging market sovereign debt is one of the most visible areas of yield advantage - – The return on the Brazilian Real Treasury debt was about 10 per cent and the return on Turkish lira bonds was about 15 per cent. While there is a risk of exchange rate depreciation, instruments such as non-proxy forward contracts (NDFs) can be used for hedge risks. At the same time, regional private credit markets are warming, especially in the Middle East and North Africa (MENA) and the Asia-Pacific (APAC) regions, and we expect more growth in the future。

Chaining is transforming traditional passive assets into proceeds-producing collateral. The bulk of monetized commodities have demonstrated market demand, with a chain size of over $4.8 billion and a total turnover of $90.7 billion as of the first quarter of 2026. Currencyized equities also show a similar trajectory, with market size increasing to over $1 billion in one year, with 185,000 holders. There are significant opportunities for any agreement that can superimpose proceeds on these assets on a large scale, whether as collateral for stabilizing currency, borrowing market assets or for option products. The potential returns are significant, as the assets are distributed on the basis of an exchange, while the returns-type position is more adhesive than the mere price exposure. The agreement to spearhead this model is expected to gain long-term holders and to build significant value over the long term。

What do we think of this market

Overall, as long as it is supported by real liquidity, monetization will create value for the encryption industry by placing real world assets in chains. While institutions and marketers still dominate and gain most of their value, future values will gradually flow to encrypted original platforms that can provide better pricing, higher returns and greater practicality. Many related infrastructure is already under construction, and we look forward to seeing more progress in the coming months。