SemiAnalysis unearthed long-term storage: $50 billion in collection, IPO in supercycle

DISMANTLING TECHNICAL PATHWAYS, FINANCIAL DATA, HBM DILEMMAS AND IPO STRUCTURES. 。

Original by Ray Wang, Myron Xie, Dylan Patel, etc

Original: Deep tide TechFlow

Introduction:CXMT is about to be listed on the science board and is expected to be the largest semiconductor IPO in Chinese history. The company, which was established only in 2016, began with the acquisition of patents and talent from the bankrupt German DRAM manufacturer, Chimunda, and made its first profit in 2025, with nearly 10 years of capital transfusions of losses tolerated by the Fatty Government, with a single quarterly collection of $7.3 billion in the first quarter of 2026. The SemiAnalysis, which has developed the technological pathways, financial data, HBM dilemmas and IPO structures, is the necessary reading material to understand the location of China’s chip storage industry。

The SemiAnalysis team was the first to describe the huge demand for the memory of AI's reasoning and intelligent workflows on the newsstream as early as the end of 2024, and has since published a number of in-depth memory reports, as well as continuous tracking of long-term storage and China's algorithmic ecology. A special in-depth study is necessary as long-term storage is about to be listed in the coming months. Longing is likely to be China’s largest semiconductor, the IPO, and will be a milestone for this Chinese head storeer. From here on out, the competition with Samsung, SK Hercules and Miracle will only increase。

Silicon Valley Returners

Founder of the stock of long coneChu YimingHe graduated from the University of Tsinghua undergraduate in physics in 1994 and then went to Stone Creek, New York State University, to study electrical engineering. He worked in Silicon Valley for many years and became the project manager of MoSys around 2001. In 2005, Chu Imin returned home with a set of SRAM patents and $100,000 seed moneyGigaDevice, later became one of the top global NOR Flash suppliers. But the global NOR Flash market is much smaller than DRAM or NAND Flash. Chu Yiming's more ambitious, he chose the DRAM track。

DRAM is not a game that Fables can play. DRAM devours capital, has strong patent barriers and is highly dependent on manufacturing capacity. By 2016, there were only three survivors of the entire industry, Samsung, SK Hercules and Misang, and 40 years of patents and capital build-up of the moat without new players. Zhu Yiming's SRAM patent and the NOR Flash business, which is prone to innovation, neither provides DRAM storage unit design nor DRAM process, much less bypassing the giant patent blockade. So the core technology had to be acquired from outside when the Chu-min and Hoi-ming municipality launched the DRAM project, Project 506 in 2016 (the later long-term storage)。

The source is a dead German company。

DRAM FOUNDATION: CHIMUNDA HERITAGE

This dead company is..QimondaI don't know. Chimunda went bankrupt in January 2009 as a result of the global financial crisis and the ensuing collapse of the storage unit, but it was a DRAM manufacturer in the head of Europe. As a subsidiary of Infinion, traced back to Siemens, Chimunda offers a scarce alternative: a deep DRAM patent bank and a storage unit architecture, both of which come from outside the Tristar-Hilness-American Triangle。

In June 2015, Polaris Innovations, a subsidiary of the Canadian patent operator WiLAN, bought approximately & nbsp from British Flying Bullshine for approximately 30 million euros;7000 Chimunda patentsAnd the application. In December 2019Polaris signed an agreement with ChangsunA lot of DRAM patents have been authorized. (a) The Yangtze High Council has publicly stated that it has received the agreement & nbsp;2.8 TB CHIMUNDA TECHNICAL DOCUMENTTHAT'S THE FOUNDATION OF THE LONG-TERM DRAM BUSINESS。

One of the key technologies that Long Sing inherited and developed from Chimunda is the 46nm level BWL storage unit (Buried Wordline)and push it to the 10nm levelI DON'T KNOW. BWL IS THE CORE ARCHITECTURE INNOVATION. THE TRADITIONAL SOLUTION WILL BE TO ACCESS THE TRANSISTOR FENCE, WHICH WILL BE WIRED ALONG THE CRYSTAL CIRCLE SURFACE, AND THE BWL, WHICH WILL SINK THE FENCE INTO THE DITCH BELOW THE BERTH LINE. THIS HAS THREE ADVANTAGES: TO REDUCE THE STORAGE UNIT TO 6F2 LAYOUT (TRADITIONALLY 8F2) AND TO EXTEND THE LENGTH OF THE DITCH WITHOUT TAKING UP THE SURFACE AREA IN ORDER TO CURB THE LEAKAGE OF THE TROUGH (IMPACT DATA MAINTENANCE) WHILE REDUCING THE FENCE-BIT-LINE PARASITIC CAPACITY. EMPLACED LINES AND STACKED CAPS, WHICH ARE THE STRUCTURES THAT ARE BEING USED TODAY BY THE THREE MAJOR STORAGE GIANTS. IT'S JUST A TECHNICAL RESERVE FOR STACKING/BWL - AND THAT'S EXACTLY WHAT THE LONG-STUFF FOUND。

Talent: from frozen blueprints to active research and development capacity

In addition to patents, the more enduring asset derived from the collapse of Yong-hoon from Chimunda is an engineer. Chimunda has a research and development centre in Xi'an with 400-500 engineers and is one of the largest research and development sites outside Germany. After the collapse of Chimunda, while the entire Sian R & D centre was taken over by the Purple Lights Group, the wider spread of talent has benefited the long-term herd。

Changsun also succeeded in attracting senior engineer Karl-Heinz Kuesters from German headquarters in Chimunda. Kuesters have been Vice President of Technology and Pre-Research in Siemens, British Flying and Chimunda for 24 years. The pre-research line he led was exactly the kind of capacitation programme — that is, the structure actually used by long-stamping. He joined as a technical adviser, EE Times, who called Kuesters the "ace" of the mackerel. Kuesters bring with them hidden knowledge (tacit know-how) that neither patent nor 2.8 TB files can carry: 20 years of experience in leading DRAM's development, so that he can tell Yong-hoon's engineers what the design is to keep, what to abandon, and how to bring the memory that runs through the lab to mass production. This integration and good judgment are not found in any patented literature。

The same pattern is true for the United States. Ping Er-xuan, Vice-President responsible for future technology assessments, is not from Chimunda, but from U.S. career in American Light, Sandisk and applied materials, and has accumulated in storage and materials technology。

There is also a large number of recruitment from South Korea and Taiwan. The Korean prosecution has indicted the former Samsung employee for leaking technology, and dozens of Korean engineers are reported to have worked in Changxi. The situation is similar in the Taiwan region, where long-standing and well-paid equipment and process engineers continue to work at the top。

THAT'S THE KEY TO UNDERSTANDING THE LONG-TERM PATH. CHIMUNDA'S PATENTS REMAIN LIMITED AND MATURE ASSETS. AND THE ABILITY TO MOVE LONG-SONG FROM G4 TO G5 TO HBM IS THE ABILITY TO PULL TOGETHER. • INDIGENOUS TALENT, CHINESE ENGINEERS RETURNING FROM WORK WITH FOREIGN FIRMS, AND A SMALL NUMBER OF FOREIGN EXPERTS — NOT DOCUMENTS. LEGACY IS ONLY THE BEGINNING, AND TALENT HAS TURNED IT INTO AN ENGINE OF AUTONOMOUS RESEARCH AND DEVELOPMENT. BUT THIS ENGINE BURNED FOR ALMOST 10 YEARS BEFORE IT MADE A PROFIT. THE QUESTION IS, WHO HAS THIS PATIENCE TO SUSTAIN BLOOD

The patience of the State

The success of the Changxiang is hardly attributable to strong support from the local and central Government of China. The City of Fatty is a classic case. "Chang Fat is China's major science, technology and innovation townPatience in the countryThe model incubates a number of successful businesses: the East of Kyoto (global head display panel manufacturer), the West (head electric car manufacturer), and now the long-term storage。

The City of Fatty has done two key things for the Changju。

First, they build local supply chains around factories. The method of adhesive play is to take a large share in the core "chain owners" and attract the rest of the chain. This is how the panel field did it to the east of Kyoto, and the electric car field did it to the east, and since 2016, the same script has been replicated for the masonry. In the vicinity of the plant, which is located in the Economic Zone of the Fatty Port, the Government has created an intensive local industrial cluster. Peyton and HYBON, the containment testing plant, are in the vicinity of a wall, with more than 99 per cent of the revenue from the HYBON. Large-scale gas plants operated by light steel supply most of the requirements of the long-term gas, and the Ziwei semiconductor under the pure-technology flag provides crystal round-recycling capacity in the high-intensity zone of the Fat New Station. The state investment also directly controls the upstream chip modelling equipment business technology。

Secondly, co-financing is willing to lose for a long time. Unlike private fund-raising funds that need to deliver returns to the LP on time, competitive State investment is ultimately supported by municipal and development area state-owned entities and does not exit the clock. They continue to give blood to a family whose first annual profit and accumulated loss was about & nbsp until 2025;RMB 36.65 billionThe company, for almost 10 years. Project 506 initiated in 2016, phase IAbout 80% of funds(14.4 BILLION YUAN) FROM CO-FINANCING. DESPITE BEING DILUTED, CO-FINANCING IN SUBSEQUENT ROUNDS OF FINANCING HAS NEVER BEEN REDUCED OR WITHDRAWN. THE LARGEST SHAREHOLDER AT IPOWe're collecting electricityShareholding 21.67%Total national investment over 30%I don't know. The willingness to treat the mill as a 10-year bet rather than a fund-cycle return — a catalyst on which both technology and talent depend。

From heritage to autonomy

Three clues come together, and the first decade of the long-term is clear. Chimunda provides a foundation: an authorized patent bank and storage unit structure from outside the giant triangle. Talent provides motivation: key figures such as Kuesters and Ping, as well as returnees from the giants of the United States, and controversial talent from Korea, who turn frozen blueprints into sustainable processes. The co-fertilizing government then provides what the first two need but cannot generate on their own: capital, patience and localized supply chains. There's no need for one。

This is followed by discussions on finance, technology and equipment ecology。

NEXT STEP IN A DECADE: IPO IN A SUPERCYCLE

THE STORY OF THE PAST DECADE, THOUGH IMPRESSIVE, IS PERHAPS JUST AN EARLY CHAPTER OF A LONGER NARRATIVE. THE COMPANY IS PREPARING TO MARKET ONE OF CHINA’S LARGEST SEMICONDUCTORS IN RECENT YEARS, POSSIBLY THE WORLD’S MOST INTERESTED SEMICONDUCTOR THIS YEAR. IN DECEMBER 2025, THE FILING OFFICE OFFICIALLY ACCEPTED THE APPLICATION FOR LISTING OF CHANG ZHENG. PRIOR TO THAT, THERE WERE PERSISTENT MARKET RUMORS IN 2024 AND 2025 THAT COMPANIES WERE PREPARING TO BE LISTED. THE MOST RECENT DEVELOPMENT WAS THE SUBMISSION OF A CVM REGISTRATION APPLICATION ON 27 MAY, WHICH IS CURRENTLY IN THE FINAL STAGES OF REVIEW。

The long-standing IPO book revealed a large amount of information previously unavailable. & nbsp of SemiAnalysis;Memory ModelThis allows for a more precise determination of the current position and future trends of the long-term sorghum。

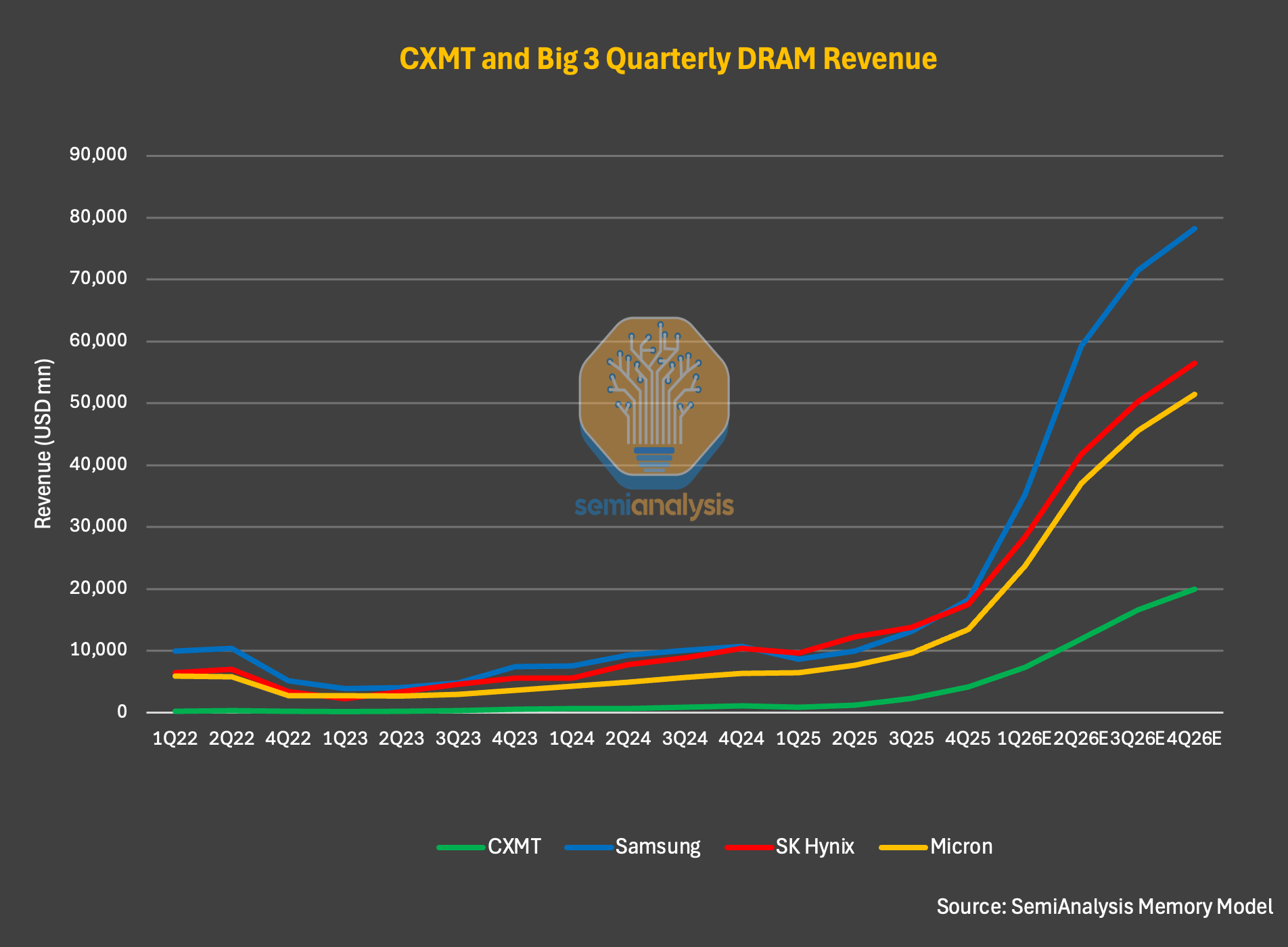

AT A HIGH LEVEL, AS MEASURED BY ALMOST ALL THE INDICATORS, LONG-TERM SORGHUM IS THE FOURTH-LARGEST DRAM MANUFACTURER IN THE WORLD AND IS INCREASING ITS LEAD AGAINST SECOND-LINE STORAGE MANUFACTURERS. THROUGHOUT THE YEAR, THERE WAS AN INCREASE OF 156 PER CENT TO APPROXIMATELY $8.6 BILLION, ABOUT $3.3 BILLION IN 2024 AND ABOUT $1.2 BILLION IN 2023. FOR THE FIRST TIME, NET PROFITS ALSO WENT UP TO $1 BILLION. EVEN SO, IN 2025, LONG-SPROUTS COLLECTED WELL BELOW THE DRAM REVENUES OF SAMSUNG (ABOUT $72.3 BILLION), SK HERCULES (ABOUT $52.1 BILLION) AND LIGHT AMERICA (ABOUT $37.2 BILLION)。

Figure: Global DRAM commercial comparison (source: Semianallysis Memoory Model)

In the first quarter of 2026, the Changsun report collected $7.3 billion, an increase of about 700 per cent over the same period, and single-season collections were close to the annual level of 2025. The operating margin also expanded sharply, reaching about 70 per cent。

SemiAnalysis thinks it's just the beginning. According to the equity book alone, the company ' s revenue collection for the first half of 2026 is projected to increase seven times over the same period, exceeding $16 billion. Throughout the year, SemiAnalysis estimated that the long-term camp could receive more than $50 billion. If achieved, this means that the company has more than doubled its revenue each year since 2023 and increased by more than six times each year in 2026。

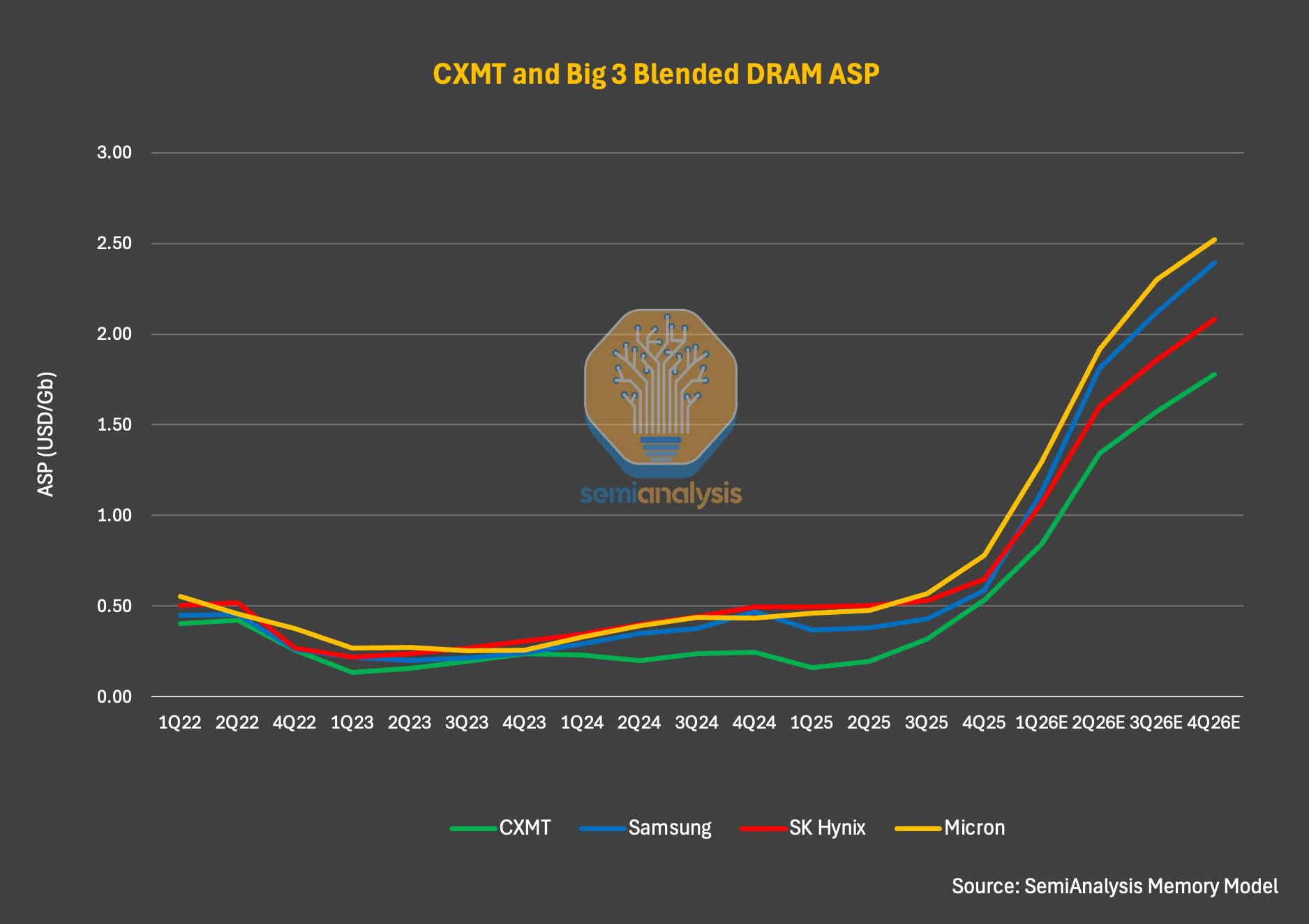

The driving force of this explosive growth is more the cycle itself than technology or market share. A closer look at the data: in the first quarter of 2026, the volume of long-term bets increased by only 11 per cent, but the ASP (average selling price) increased by about 57 per cent, following the previous increases of 63 per cent in the third quarter of 2025 and 68 per cent in the fourth quarter. The real push was for explosive price increases rather than a significant seizure of market shares for peers. In terms of bit output, the SemiAnalysis model shows that the market share of long-term snails will increase from 9 per cent in 2025 to 12 per cent in 2027. Three percentage points of the growth appears modest, but it is significant in a market that Semianallysis predicts to be close to $1 trillion in 2027。

Figure: Trends in ASP and bit deliveries from CXMT (source: SemiAnalysis Memoory Model)

The error in the story about the China Stores

A more interesting finding for readers who have not yet followed the long-term or storage markets in depth is the comparison of long-term pricing with industry leaders. Based on Memory Model’s data, the long-standing DRAM ASP challenges a common misconception: China’s memory is more structurally cheap, shocks markets and lowers global prices. This may have been true in some cases in the past, but it is not accurate in the current cycle。

In the first quarter of 2026, for example, DRAM ASP is only about 5-10% lower than Samsung, SK Hercules and American Lights. SemiAnalysis expects that this direction will not change throughout 2026, but the gap will widen. The reason for this increase is not inherent price differentials, but changes in product structure. DRAM and HBM servers account for a higher proportion of deliveries, while DRAM servers offer better pricing prospects than consumer-grade DRAM。

By the end of 2027, SemiAnalysis expected servers DRAM and HBM to account for more than 50 per cent of DRAM terminal market demand. Due to the higher unit price per GB for servers DRAM and HBM, the head manufacturer will further widen the gap with the long-stamper on the ASP, especially in view of the anticipated substantial increase in HBM prices in 2027。

Figure: DRAM manufacturer ASP comparison (source: SemiAnalysis Memory Model)

Profit margin: periodic gifts

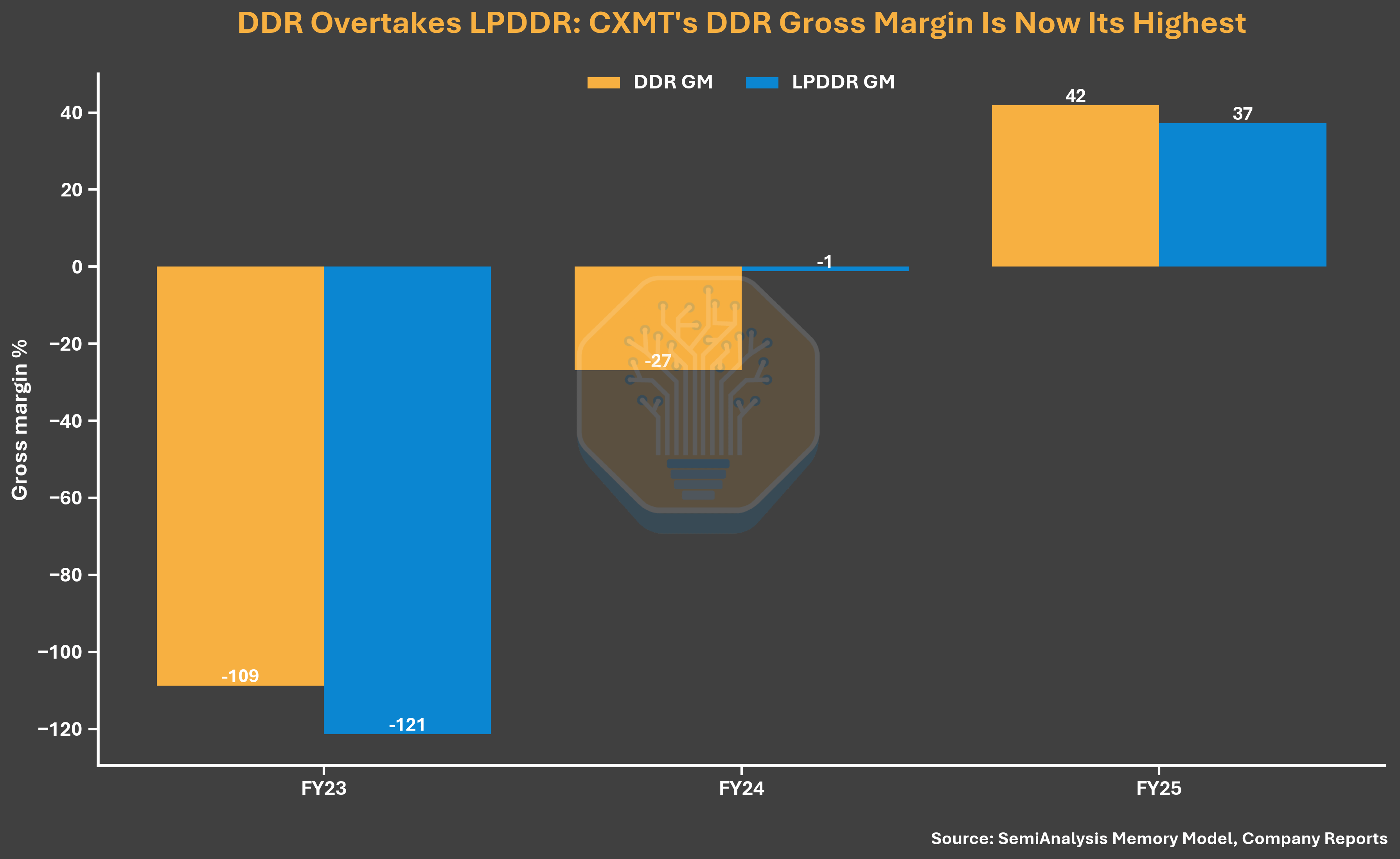

THE STRONG ASP WIND HAS SIGNIFICANTLY IMPROVED THE PROFITABILITY OF LONG-SPRING. THE MĀORI RATE REACHED 37.8 PER CENT THROUGHOUT THE YEAR, CLOSE TO 39.4 PER CENT OF SAMSUNG AND 39.8 PER CENT OF U.S. LIGHT, BUT FAR BELOW 60.4 PER CENT OF SK HERCULES (SK HERCULES BENEFITED FROM A HIGHER HBM DELIVERY). THE MĀORI RATE OF ABOUT 38 PER CENT, RELATIVE TO -113 PER CENT IN 2023 AND -4.7 PER CENT IN 2024, WAS A HUGE LEAP FORWARD. THE YEAR 2025 WAS NOT ONLY THE HIGHEST IN HISTORY, BUT ALSO THE FIRST TIME THAT A COMPANY HAD ACHIEVED POSITIVE MĀORI。

Figure: Comparison of Māori rates for DRAM manufacturers (source: Semianallysis Memoory Model, company report)

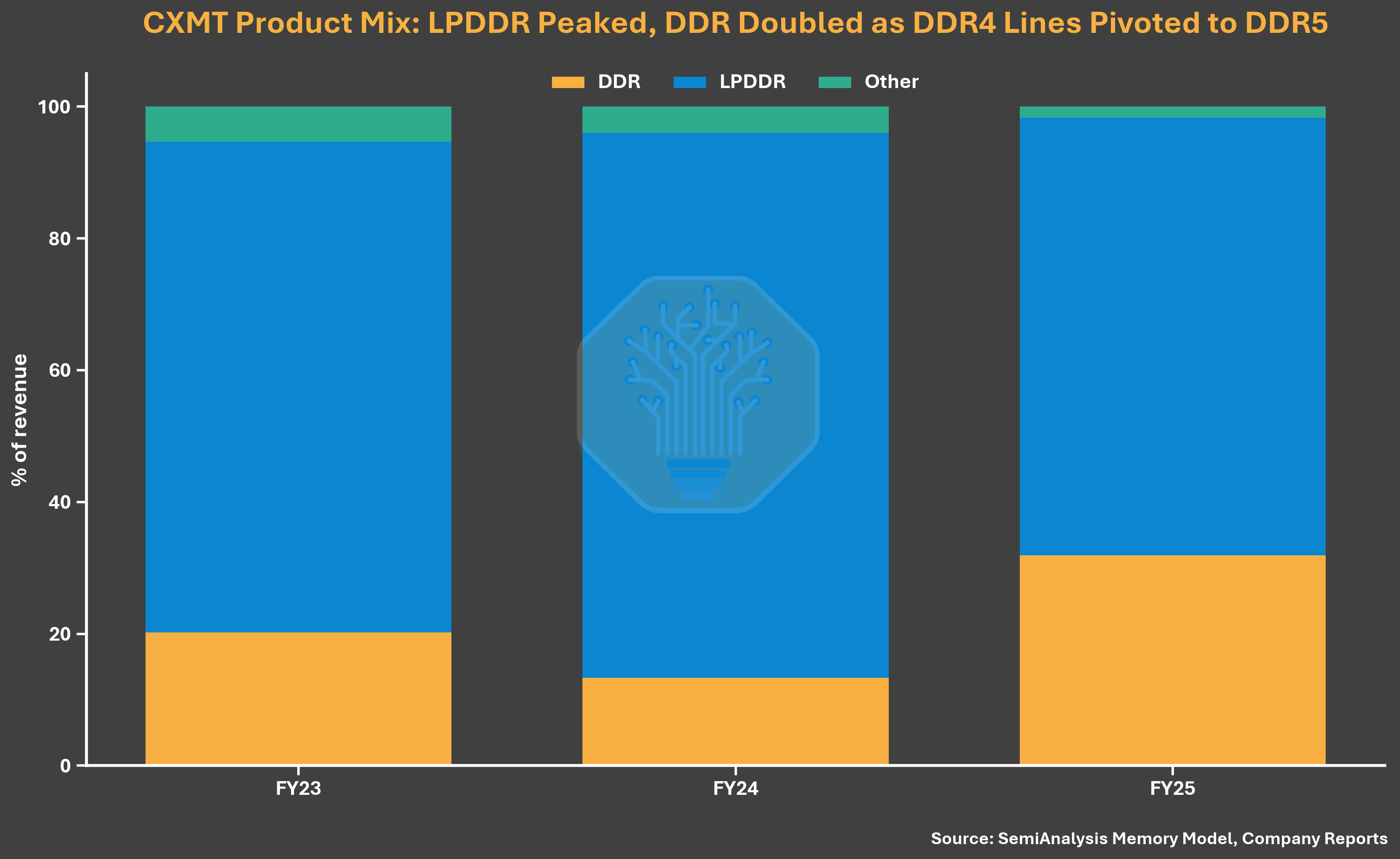

In 2026, the profitability improved further. The operating profit margin reached 70 per cent in the first quarter, with SK Hercules 73 per cent, Samsung 81 per cent and American light 84 per cent over the same period. In addition to ASP growth, the increase in long-term profit margins is also due to its almost exclusive focus on the product structure of large-scale DRAMs, which are actually higher than HBMs in the current environment. According to the equity book, approximately 99 per cent of the company ' s bits in 2025 were traditional LPDDR and DDR products, and HBM contributed minimally to the revenue and profits。

Figure: Comparison of margins of operations of DRAM manufacturers (source: Semianallysis Memoory Model, company report)

A simple DDR5 unit cost analysis makes the picture clearer. SemiAnalysis found that the DDR5 per bit cost of long swirling is still over 30% higher than the three giants. But since the DDR5 prices were already very strong in the first quarter of 2026, the Mauricity Rate of Long Seng has been pushed to over 70%. This means that the improvement of long-term profit margins is driven mainly by pricing rather than by a substantial increase in product competitiveness or cost structure。

Figure: DDR5 cost comparison per bit (source: SemiAnalysis Memory Model)

Productive expansion: approaching beauty light

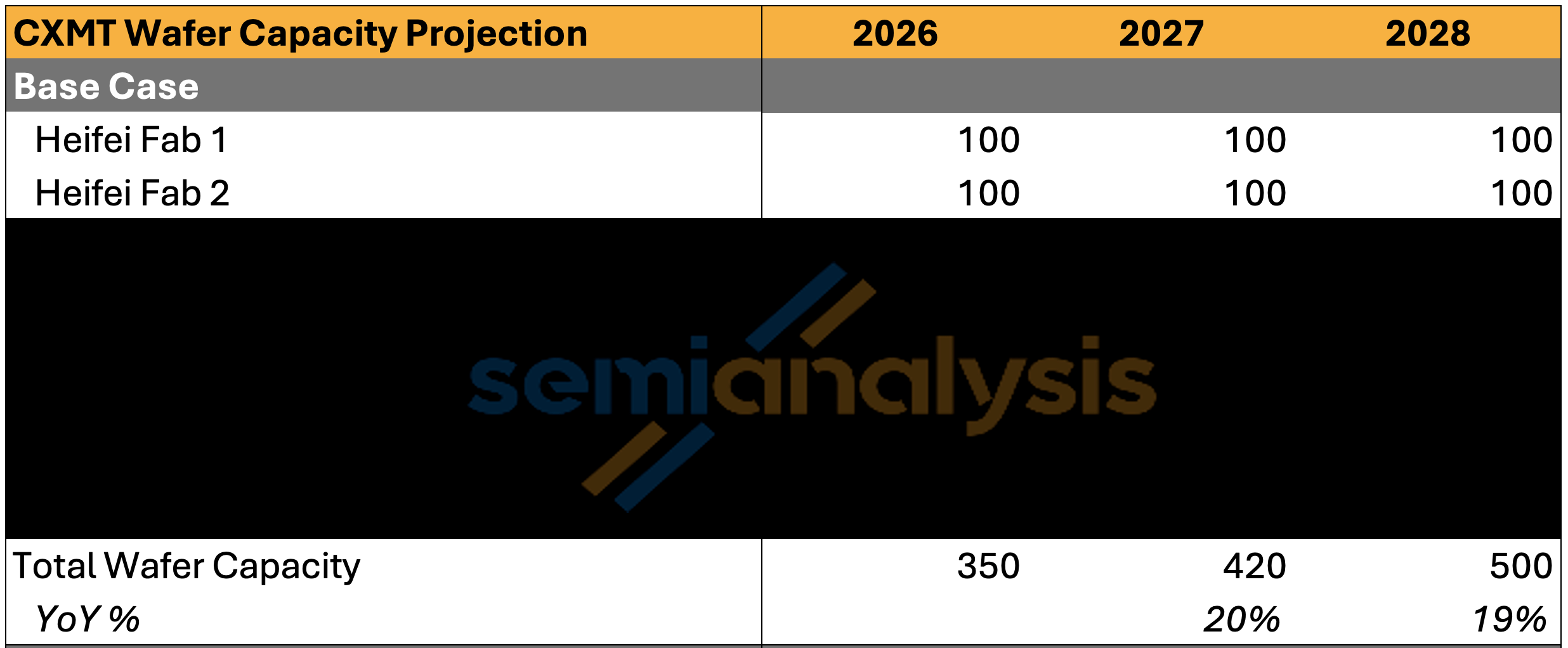

In addition to record profits, long-term maggots are catching up with capacity. By the end of 2026, SemiAnalysis is expected to reach approximately & nbsp;350,000 films/months& nbsp;38.5 000 films/monthsI don't know. In order to rank by crystal round capacity, long-term sorghum is expected to be the third largest storeer in the industry。

Figure : Global DRAM manufacturer ' s round-month power comparison (source: SemiAnalysis Memory Model)

however, there is still a significant gap between the long and the two giants: samsung & nbsp;720,000 films/monthsSK Hayrist & nbsp;59.5 000 per monthi don't know. by 2027, with the first phase of shanghai ' s initial climb and compost, and the full production of beijing, the long-lived production capacity could reach & nbsp;About 42 000 films/months& nbsp, the global DRAM capacity;17%, above approximately & nbsp in 2025;13%i don't know. based on the volume of bet deliveries, the share is from & nbsp in 2025;9% to 2027;12%I don't know。

By 2028, with full production and two periods of continuous climb in Shanghai, SemiAnalysis is expected to reach 500,000 tablets/months, representing about 17 per cent of the global supply of DRAM。

Figure: CXMT co-fertiliser area capacity (source: SemiAnalysis Memoory Model)

Fear of oversupply: no fear for at least two years

Given the increasingly important role of long-term sorghum in global DRAM capacity, investors, as in each of the previous cycles, are concerned that Chinese manufacturers may create supply-demand imbalances. SemiAnalysis believes that this concern will be over-expanded in the next two years at least. After including the incremental capacity of long-stamp and other storage plants and the delivery of bits, the supply of DRAM remains extremely strained, assuming a utilization rate of over 90 per cent。

Figure: DRAM supply and demand balance (source: Semianallysis Memoory Model)

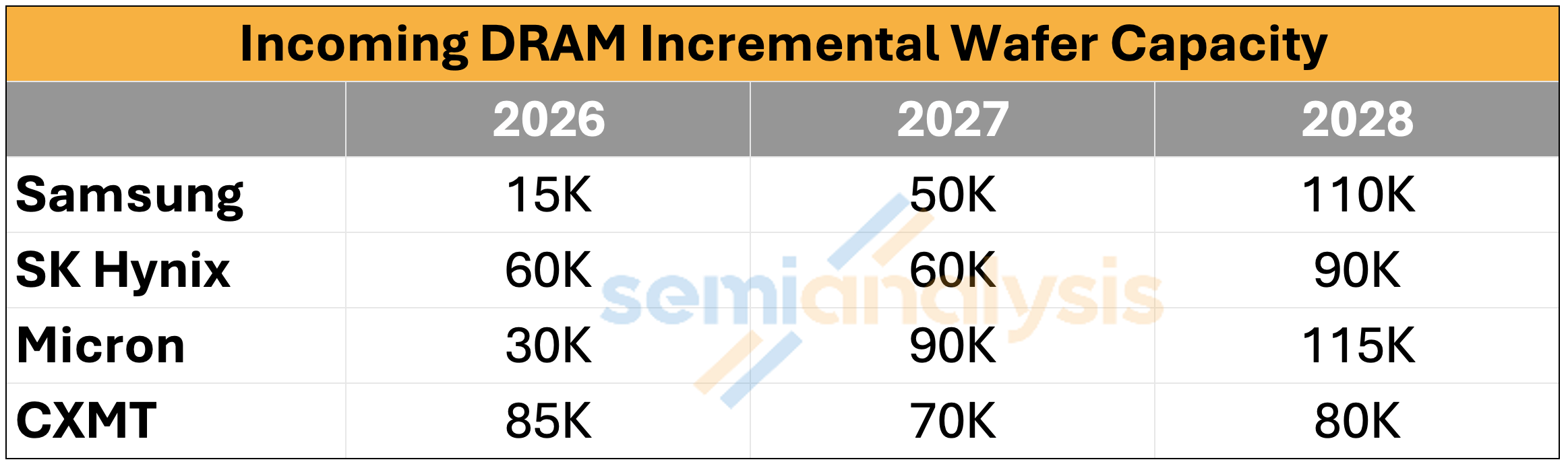

A single look at the energy expansion rhythm of long sorghum: around 85,000, 70,000 and 80,000 new episodes/months were added each year in 2026-2028, while the three stars were 15,500 and 11,000, SK Hercules 606,000 and 99 thousand, and U.S.S. 30,000/90,000/1115. Even taking these additional capacities into account, DRAM will still be short of a high-digit percentage in 2026, and the gap in 2027 will be widened to a low to medium-digit percentage. SemiAnalysis has previously elaborated on why DRAM may continue to be in short supply until 2028。

It is not the ability of the long cone to unreasonably accelerate the expansion of its capacity to disrupt the market beyond the current rhythm, as the crystal-turner plant has a long construction cycle. The current extremely favourable pricing environment is the main driving force behind the outbreak of long-term performance. Of course, Changsun wants this environment to continue. The progress in the construction of the Cyclops plant, tracked by SemiAnalysis, also shows no signs of this possibility, but it should be stressed that the total Cyclops capacity in the Shanghai plant area can exceed 400,000 units/months at full production。

HBM: THE PILGRIM FAULT

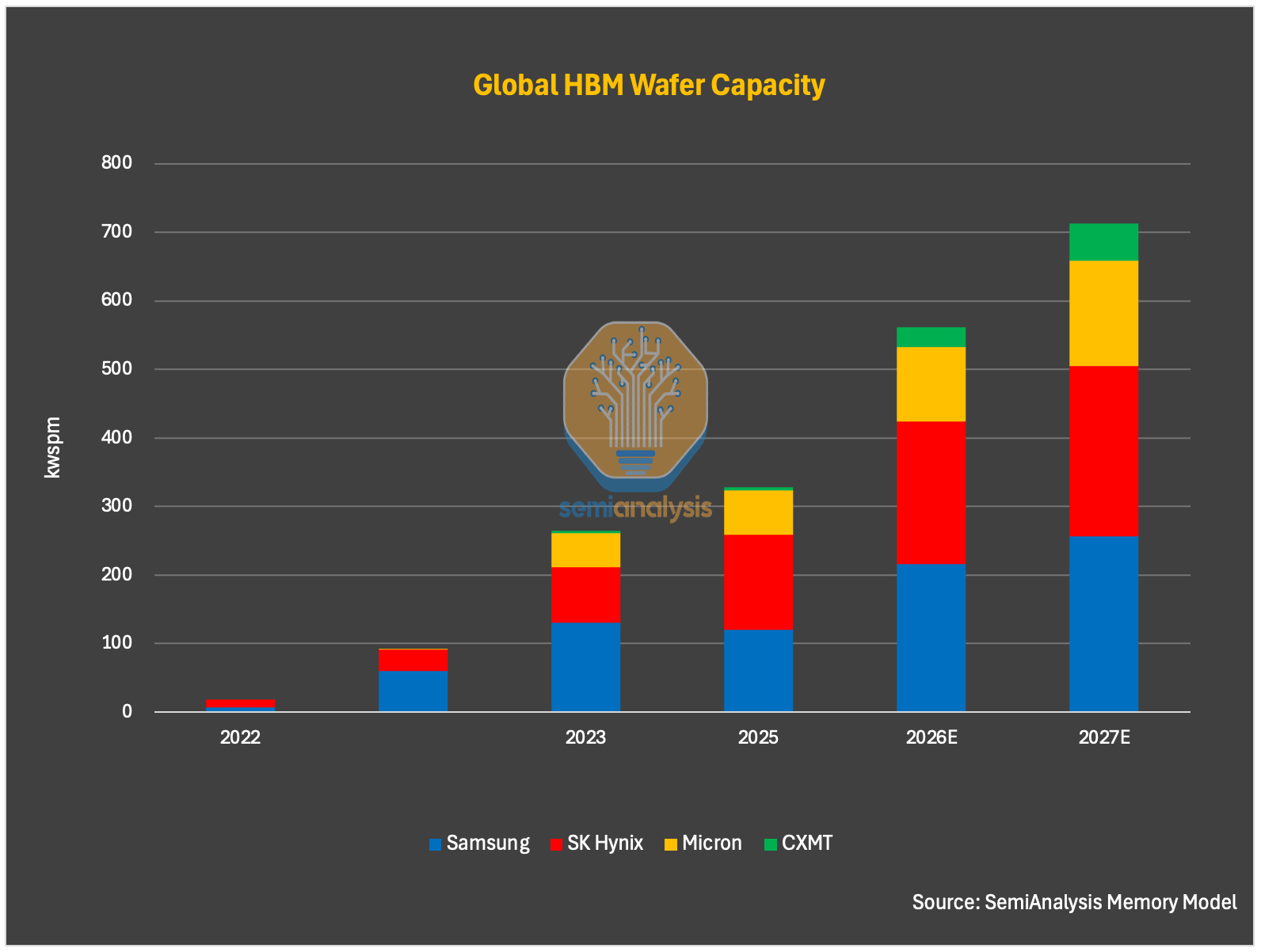

For HBM, the distribution of long-chick crystals is very limited. By the end of 2025, only about 5,000 of the approximately 2.65 million tablets per month had been allocated to HBM. The number is expected to increase to about 30,000 by the end of 2026 and about 55,000 by the end of 2027. This is consistent with the disclosure of approximately 99% of the share book collections from DDR and LPDDR in 2025。

Figure: CXMT HBM Crystal round energy distribution (source: Semianallysis Memory Model)

However, this distribution pattern may change. China ' s drive for AI ' s autonomy and control may conflict with corporate business priorities, and it is expected to increase over time. SemiAnalysis has included in its projections government-directed pro-HBM energy, which is expected to expand faster in 2027 and 2028. Anticipated HBM capacity reached & nbsp in 2027;5.5 million films/months& nbsp in 2028;100,000 films/months& nbsp in 2025;1% to 2028;12%I don't know。

It is important to bear in mind that, unlike other storage manufacturers, long-term sorghum is not only an economically and technically important company, but also a strategic asset that countries can use to advance priority policy objectives。

In short-term business logic, it is reasonable to prioritize the distribution of capacity to large groups of DRAMs over HBMs. Large-scale DRAMs currently have a significantly higher profit margin than long-lived HBM products and have more than three times the output of HBM under the same crystal area. At a stage where HBM technology is not yet mature, a large investment in HBM capacity will consume scarce crystal round capacity that could otherwise be used for higher profitability and larger volumes of output. But China must push forward with HBM layouts, because HBM sales to China are severely restricted by United States export controls, and South Korean manufacturers only maintain their exports to China through loopholes。

HBM TECHNOLOGY GAP

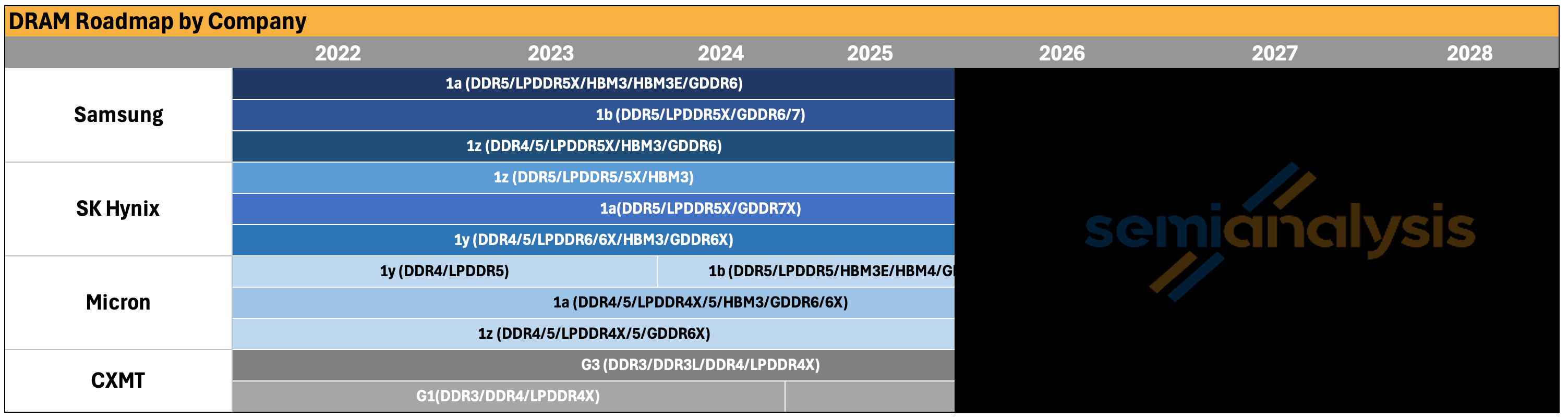

In terms of technical readiness, SemiAnalysis considers the long-sprout still to be & nbsp;HBM3 8-hi struggles for stability of production12-hi faces greater challenges。

On the front track, Long Sing made progress in its production stability **G4 (Equivalent 1z node)** and most DRAM outputs will be based on the G4 process in 2026. However, the DRAM core chip for HBM should be significantly lower than the bulk DRAM due to the larger strip size and stricter performance requirements. SemiAnalysis believes that the positives ahead remain a major challenge and that the gap with peers remains wide. Despite the increase in the G4 rate, it is assumed that the lower profitability rates in 2024 and 2025 may still fall below the 85-90 per cent maturity rate of the 1z node industry standard. This implies that equipment restrictions and manufacturing experience remain continuing obstacles that need to be overcome。

Figure: Road Map and Good Rate for CXMT DRAM Node (source: SemiAnalysis Memory Model)

The next generation process node G5 (Equivalent 1a) can theoretically continue without relying on the EUV optical carving machine as the 1a of beauty, but will face growing manufacturing and design challenges. These challenges are exacerbated by the application of this node to the HBM ' s nudity。

Naked piles are the biggest obstacle to long-standing HBMs. HBM stacks usually pose serious technical difficulties: heat stress, nudity cracks, warp, bond defects, and loss of a good rate of multiple layers of stacking. These problems are even more acute when moving from HBM3 8-hi to HBM3 12-hi and even HBM3E, as experience with the manufacture of long-sprouts at 12-hi and above is still insufficient。

The collage is not unique. The head manufacturer also faced problems of fragmentation, heat management and good rate loss on 12-hi HBM4. 16-hi and even 20-hi are more difficult - Rubin Ultra is expected to adopt 12-hi HBM4E instead of 16-hi because of supply: 16-hi needs more DRAM crystals, more difficult to manufacture, more thinning and less efficient bit supply。

SemiAnalysis believes it is increasingly possible to skip HBM3, focusing directly on HBM3E 8-hi and 12-hi. There are two reasons: first, clients need more competitive HBM products in the 2027 time window; and second, mainstream accelerators will carry HBM3E, HBM4 and HBM4E。

Figure: Global HBM road map comparison (source: Semianallysis Memoory Model)

WITH RESPECT TO BACK-WAY SEALING, ALTHOUGH THE USE OF MR-MUF OR TC-NCF REMAINS CONTROVERSIAL, THE CHALLENGE OF SEALING IS RELATIVELY MORE MANAGEABLE, AS COMPANIES AND THEIR SEALING PARTNERS ARE LESS RESTRICTED UNDER EXPORT CONTROLS. LONG-SONG HAS BEEN WORKING CLOSELY WITH HEAD OSAT, SUCH AS TON-RICH MICROPOWER, AND BACKWAY CAPACITY SHOULD BE GRADUALLY IMPROVED, BUT THERE IS STILL A GAP WITH HEAD STORAGE MANUFACTURERS。

Based on existing manufacturing challenges, Semianallysis modeled the fore and foreground rates of HBM3 8-hi at about 35% and 70%, respectively, and the combined good rate at only about & nbsp;25%I don't know. HBM3 12-hi or HBM3E 12-hi should have a lower combined good rate due to greater difficulty of stacking and keying. At this positive level, the same crystal round capacity, with long-term HBM output, is much lower than that of the head manufacturer. More critically, output HBM margins are extremely low, especially when compared to large numbers of DRAMs in the current pricing environment。

The plight of long-standing HBM is also reflected in the penetration of its products. SemiAnalysis believes that only Chinese, Cold War and a few emerging Chinese AI chip start-ups may adopt long-lived HBMs, although the rates may be high. Domestic AI accelerators still tend to use foreign HBM3 and even HBM3E, whether through any available channels or prior to export controls in December 2024. As China’s domestic cloud producers’ capital spending and capacity-building grew rapidly, so did the domestic production of HBM demand。

A NOTABLE EXCEPTION IS HBM, WHICH WILL BE DEVELOPED NOT BASED ON JEDEC STANDARDS AND PHY, WHICH WILL HELP COMPENSATE FOR BANDWIDTH DISADVANTAGES。

THE HBM SUPPLY CONSTRAINTS THAT CHINA IS FACING MAY BE MORE SEVERE THAN WHAT IS IMPLIED BY THE SLOW DEVELOPMENT OF THE HBM ITSELF. THE SUPPLY OF THE THREE MAIN HBM SUPPLIERS IS INHERENTLY TIGHT AND, UNDER UNITED STATES EXPORT CONTROLS IN DECEMBER 2024, THEY HAVE BEEN RESTRICTED TO SALES OF HBM2E AND MORE ADVANCED HBM PRODUCTS TO CHINA. IN A TIGHT SUPPLY ENVIRONMENT, THESE MANUFACTURERS ARE LESS WILLING TO VENTURE AGAINST CHINESE SALES。

However, the situation is complicated by HBM transit and smuggling. SemiAnalysis learned that some Chinese companies are still accessing HBM3 through various channels. Transit through overseas offices or third-country partners remains a route; some third-country OSAT or middlemen are also facilitating these flows. Some of the entities exported in the form of incomplete systems or modules (not considered finished GPU or ASIC and therefore still allowed to be exported to China), and HBM was then dismantled and resealed to the national GPU or ASIC。

THE IPO STRUCTURE REVEALS SOMETHING

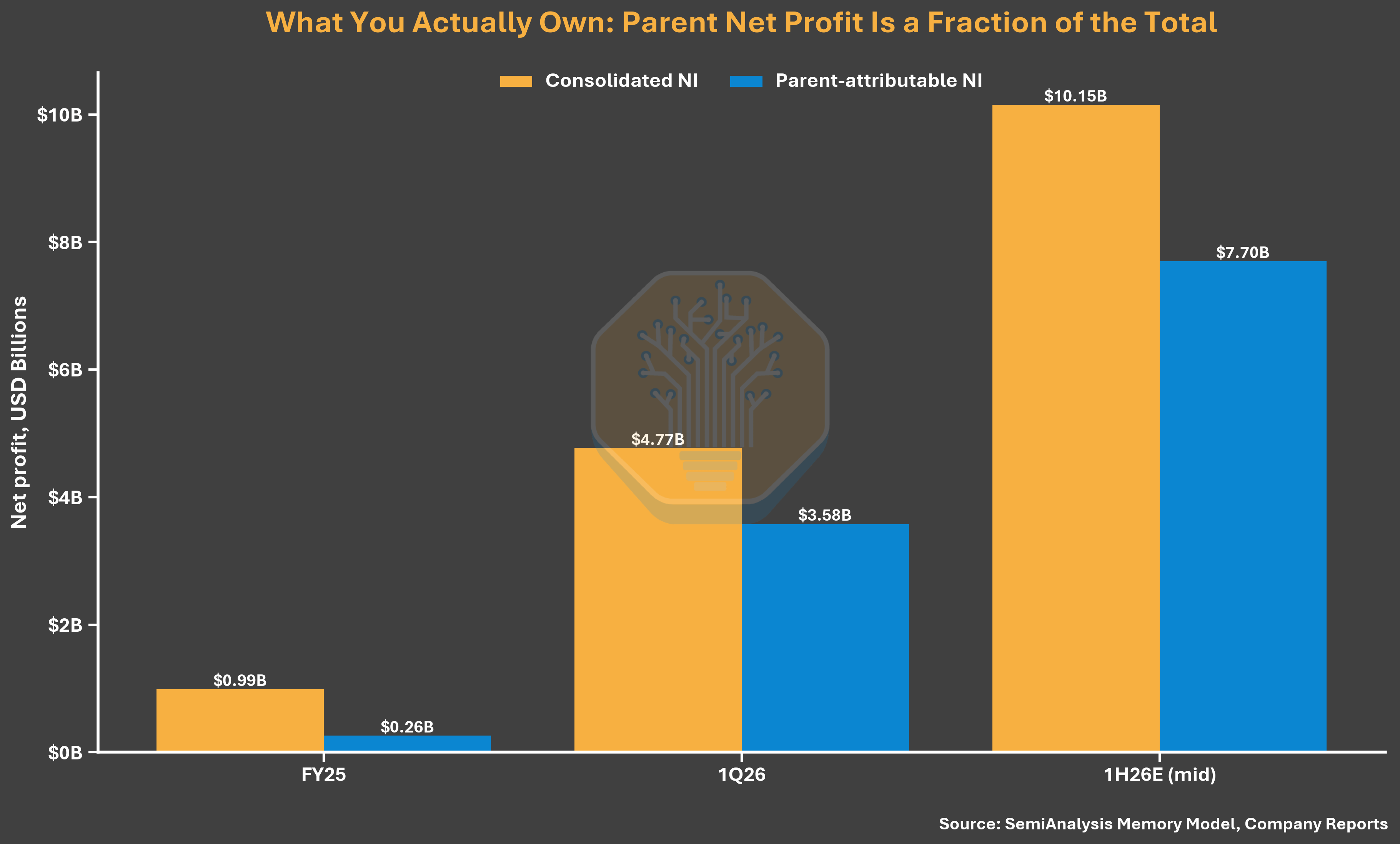

LONG-SHIN MAY BE ONE OF CHINA’S LARGEST SEMICONDUCTORS, AND ITS EQUITY STRUCTURE IS MORE NOTEWORTHY THAN BOOK-BASED FINANCIAL DATA. IN 2025, THE CHANGSUN REPORT NET PROFIT FROM CONSOLIDATION OF RMB 71.44 BILLION, BUT THE NET PROFIT ATTRIBUTED TO SHAREHOLDERS IN THE PARENT COMPANY IS ONLY RMB 18.77 BILLION, WITH 74 PER CENT ATTRIBUTED TO MINORITY SHAREHOLDERS。

This is due to the equity structure. Long-term Chang-Sung Bridge only holds 30,68 per cent economic interest and 31.72 per cent economic interest in Chang-sung Beijing, but controls 73.01 per cent and 75,32 per cent of voting rights, respectively, through long-term concerted action arrangements. This has allowed companies to consolidate most of their virtually unowned round mills, and the combined data therefore overestimates the actual profits that public shareholders actually earn by about four times。

Figure: CXMT combined profits vs. mother ' s profits (source: Semianallysis Memory Model, company report)

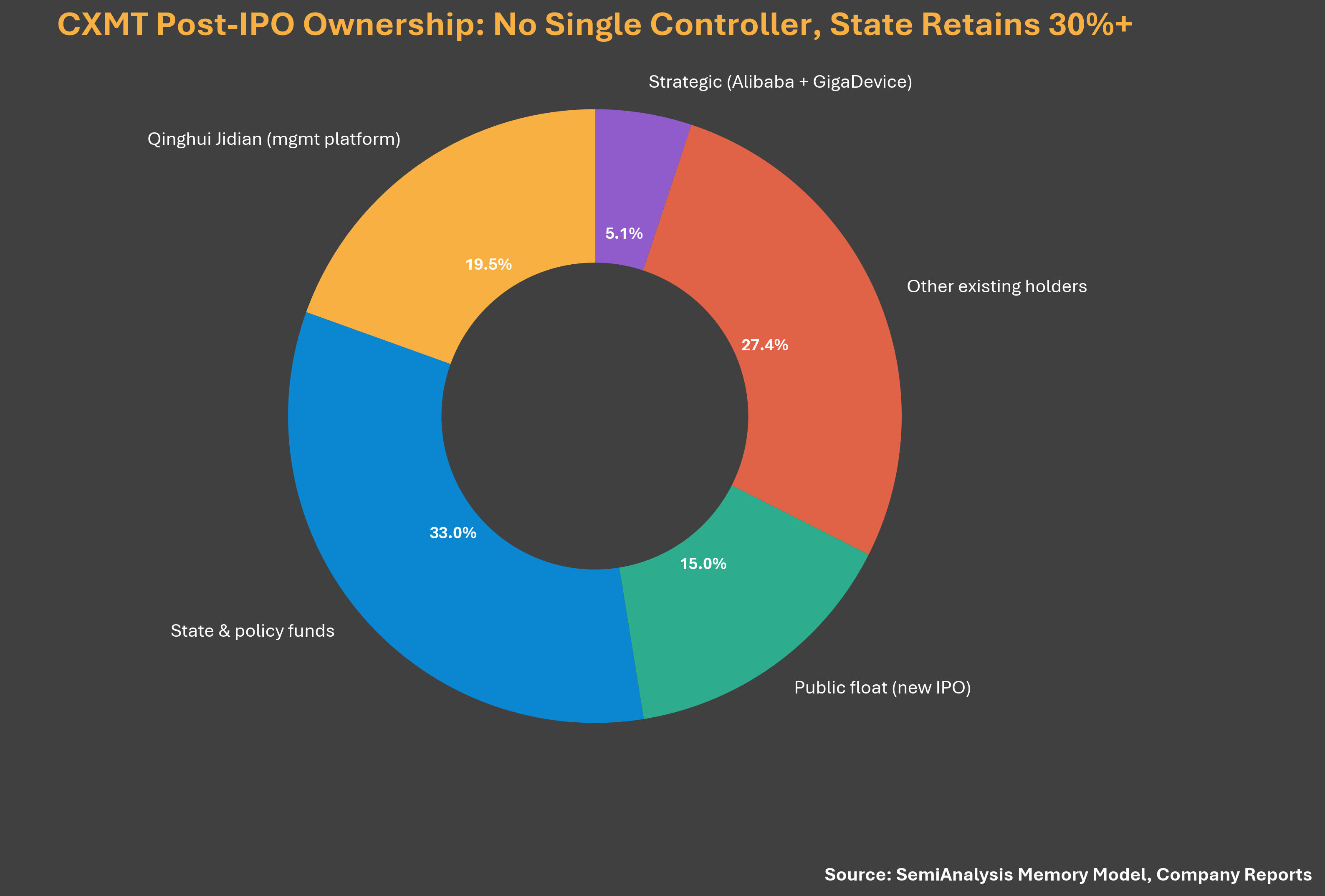

The same voting structure also makes the company's statements of “uncontrolled shareholders, de facto controlrs” unconvincing (which are listed in the book as formal governance risks). Through a unanimous operator agreement, Chang Zheng exercised majority voting control over the Crystal Circle plant, and the National Investment Fund for Integrated Circuit Industries, Phase II, Fatty and Anhui, the State-owned entity, had a combined share of well over 30 per cent since its listing. This arrangement appears to be aimed at regulating export controls and foreign investors' perceptions, at a time when the relationship between Changxi and the Chinese Government is most under scrutiny。

Figure: CXMT stock structure (source: Semianallysis Memoory Model, company report)

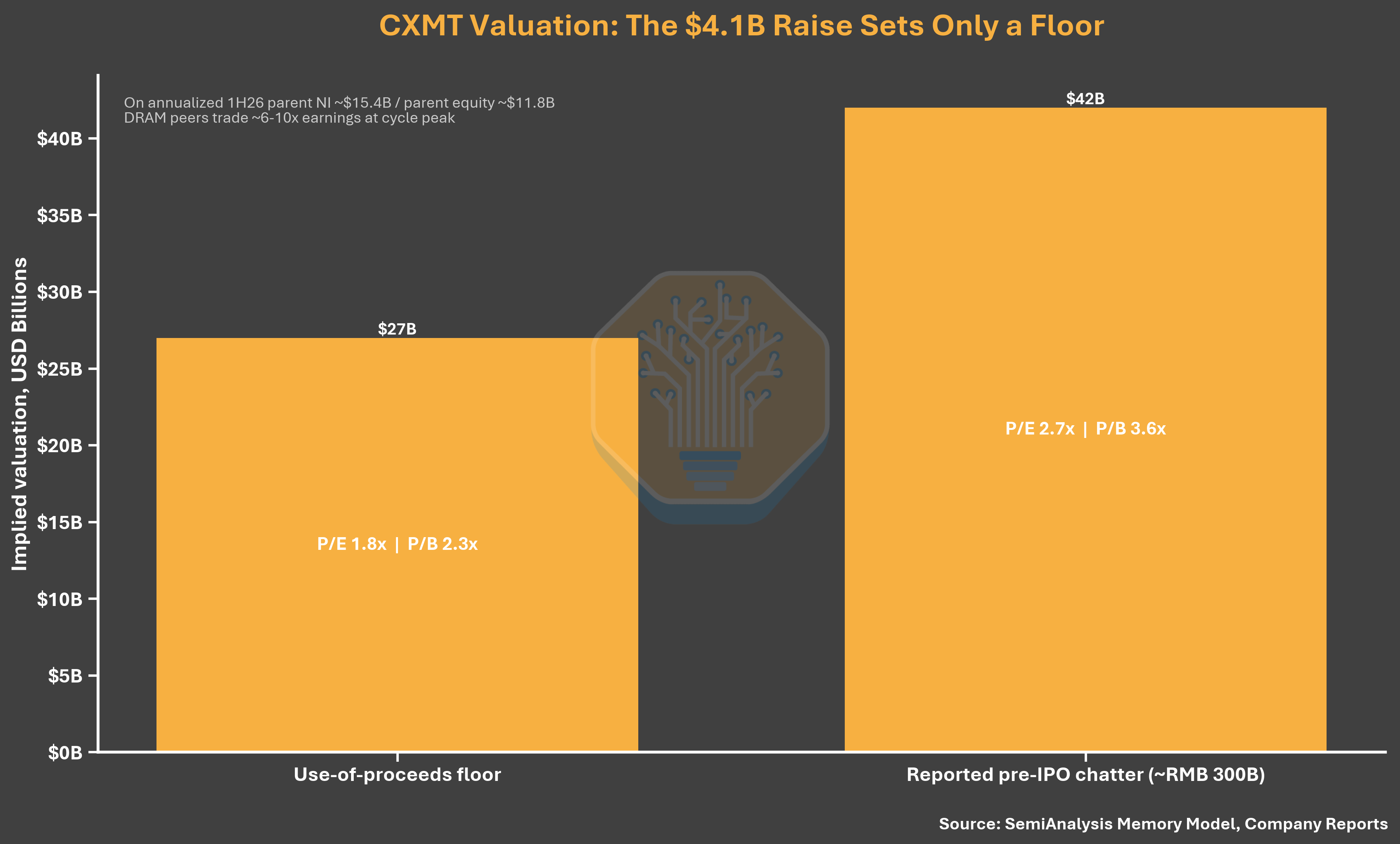

Valuation: Undervalued floor

The Changsung project collects 29.5 billion yuan (approximately $4.1 billion) of the total equity of 10-15 per cent after its publication. Full IPO financing means: about $4.41 per share at 10 per cent dilution and about 2.78 per share at 15 per cent dilution (at $2.63 in June 2025). Low-end prices were almost non-existent compared to the previous round, although $7.3 billion in revenue and $4.8 billion in net profits were realized in the first quarter of 2026. 2.78 The equivalent of approximately $7.7 billion (approximately $27 billion) is only 1.8 times the annualized return of profits to the mother in the first half of 2026. SemiAnalysis argued that the valuation floor was too low and that the actual pricing should be much higher。

Figure: CXMT IPO valuation analysis (source: Semianallysis Memory Model, company report)

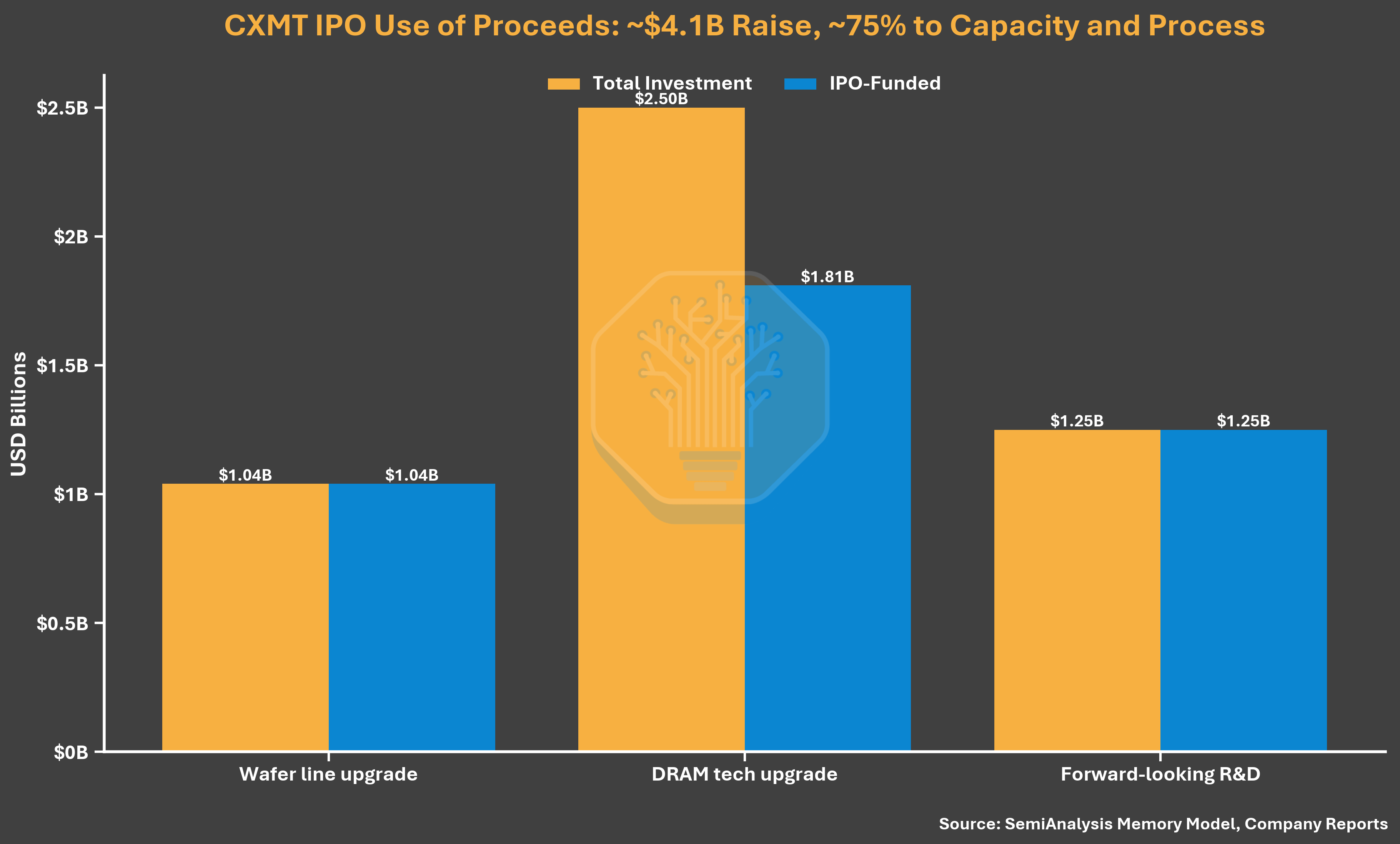

FUND-RAISING: FOCUSED DRAM, NOT HBM

THE FUND-RAISING OF $29.5 BILLION HAS REINFORCED THE CURRENT PRIORITIES OF CHANGO. OF THIS AMOUNT, 20.5 BILLION YUAN (69.5 PER CENT) WAS SPENT ON THE UPGRADING OF THE CRYSTAL CIRCLE AND DRAM TECHNOLOGIES AND 9 BILLION YUAN (30.5 PER CENT) ON FORWARD-LOOKING DRAM STUDIES. THE EQUITY BOOK DID NOT DISCLOSE A SPECIFIC HBM PROJECT OR EVEN MENTION HBM. THE PROJECT DESCRIPTION FOCUSES ON THE MIGRATION OF UPDATED PROCESS PLATFORMS, PRODUCT ITERATIVES AND EXISTING PRODUCTION LINES TO THE MEDIUM-HIGH END DRAM. THE CENTRAL ROLE OF THE IPO IS TO STRENGTHEN THE DRAM MANUFACTURING AND TECHNOLOGY BASE OF THE LONG-STANDING, WITHOUT OPEN FINANCIAL COMMITMENT TO THE RECENT HBM EXPANSION。

Figure: CXMT IPO fund-raising allocation (source: Semianallysis Memoory Model, company report)

Warning on the timing of the cycle

THE MARGIN OF PROFIT MOVEMENT REQUIRES A REMINDER ABOUT THE TIMING OF THE CYCLE. IN DECEMBER 2025, CHANGSUN EXPECTED TO LOSE A LOSS OF 6-16 BILLION YUAN FOR THE WHOLE YEAR. AN UPDATED EQUITY BOOK FIVE MONTHS LATER REPORTED A PROFIT OF $1.87 BILLION, MORE THAN DOUBLE THE PREVIOUS HIGH-END ESTIMATE. THIS ALSO SHOWS HOW QUICKLY DRAM TOP PRICING CAN CHANGE THE VALUATION DENOMINATOR - BOTH IN THE SAME DIRECTION。

Ali Baba's double role

The last detail: Ali Baba's role in the long-term stockholders' list has changed the interpretation of long-term demand. Ariyun is both a core super-large client and close to 4 per cent of shareholders and endorsements, alongside Chu's sign of innovation (about 1.8 per cent). The domestic demand level is to some extent guaranteed, which is an advantage that the Korean giants did not have in their own markets. The percentage is small and much more significant。

Note: The in-depth analysis of the ecological aspects of CXMT equipment, the impact of export controls, Chinese storage and calculus ambition in the latter part of this paper is SemiAnalysis and is not included in this translation。